Music Rights Report 2025

28.08.2025.15 min read

28.08.2025.15 min read

This is the second installment of our series, and also the second part of Andres Lauer’s Keynote at the Sonar Festival 2025. In this presentation we look closer at the music rights market, which contains publishing and master, Frontline and Catalog. We explore the current developments that are shaping how we produce, distribute, consume and especially discover and market music.

The series:

For this report, we have used a combination of public data, partner data sets (some of which must remain confidential), expert interviews, and our own research to develop the insights and projections presented. The focus is primarily on Western markets and countries considered developed by industrial and technological standards. The Global South, with its own dynamics and opportunities, will be covered in a separate study later this year.

This report is not intended as an academic publication. Instead, we have prioritized usability and strategic relevance. Our research is supported by private client data, benchmarking against industry reports, and insights from leading analysts across the music and entertainment sectors.

We’re seeing a set of long-term trends in the music industry that are increasingly reflected across the broader entertainment space. New technologies are reshaping user behavior—how we consume media, how we interact with it, and how much space and attention it commands.

At Outpost, we’ve been tracking these changes over the last 12–24 months, and we Identified three main areas:

To understand the shift in music consumption, we analyze streaming data from digital service providers (DSPs), with a focus on Western markets. For additional context, we cross-reference this data with broader trends in digital entertainment, including short-form content consumption on platforms like TikTok and YouTube, media device usage, and demographic characteristics.

We use the following definitions:

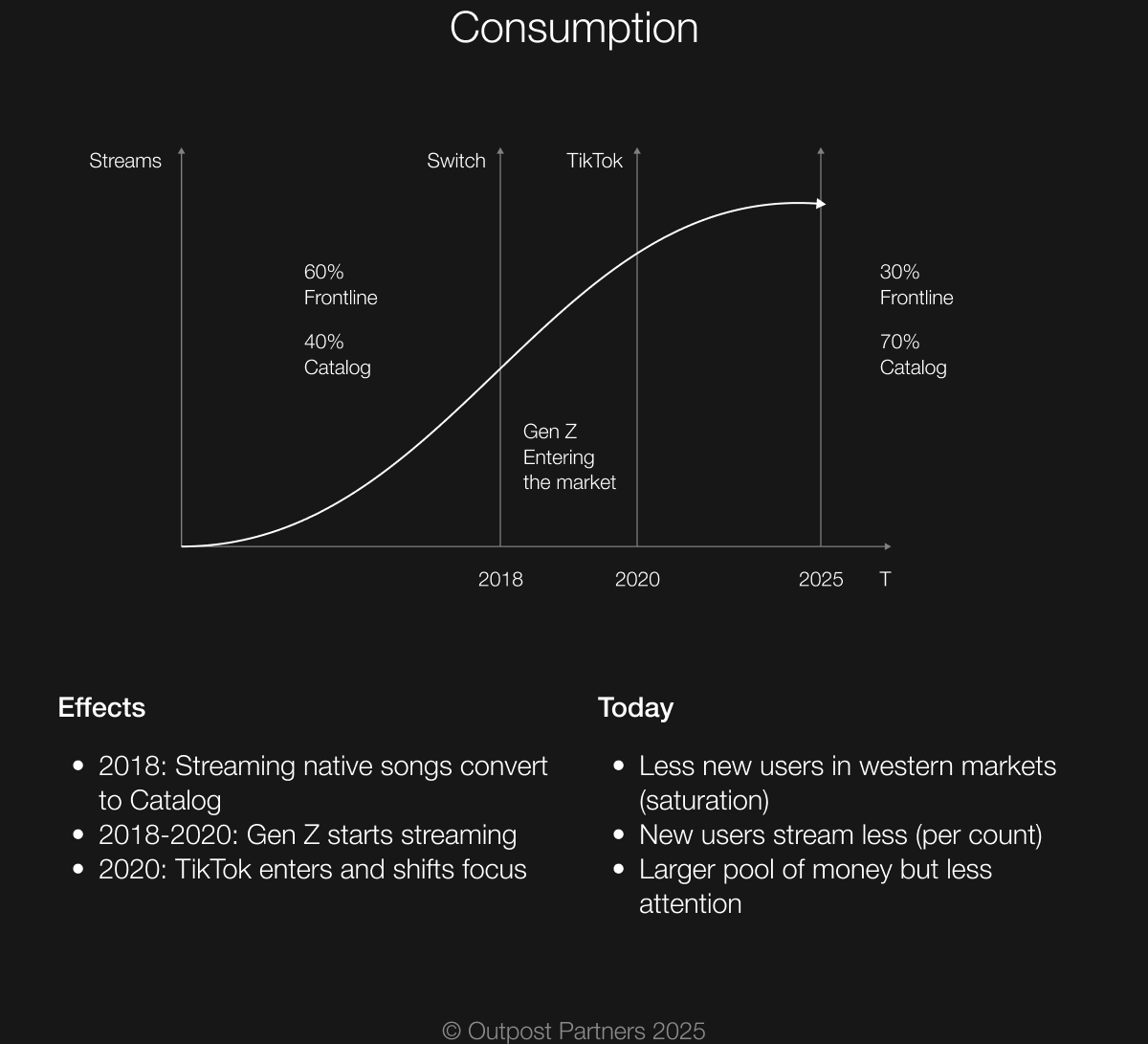

The first wave of music DSPs emerged around 2008, when platforms like Deezer, Spotify, and SoundCloud began offering access to limited music repertoire to users. A second wave followed around 2015, led by larger incumbents such as Apple Music and YouTube Music, alongside local players in regional markets.

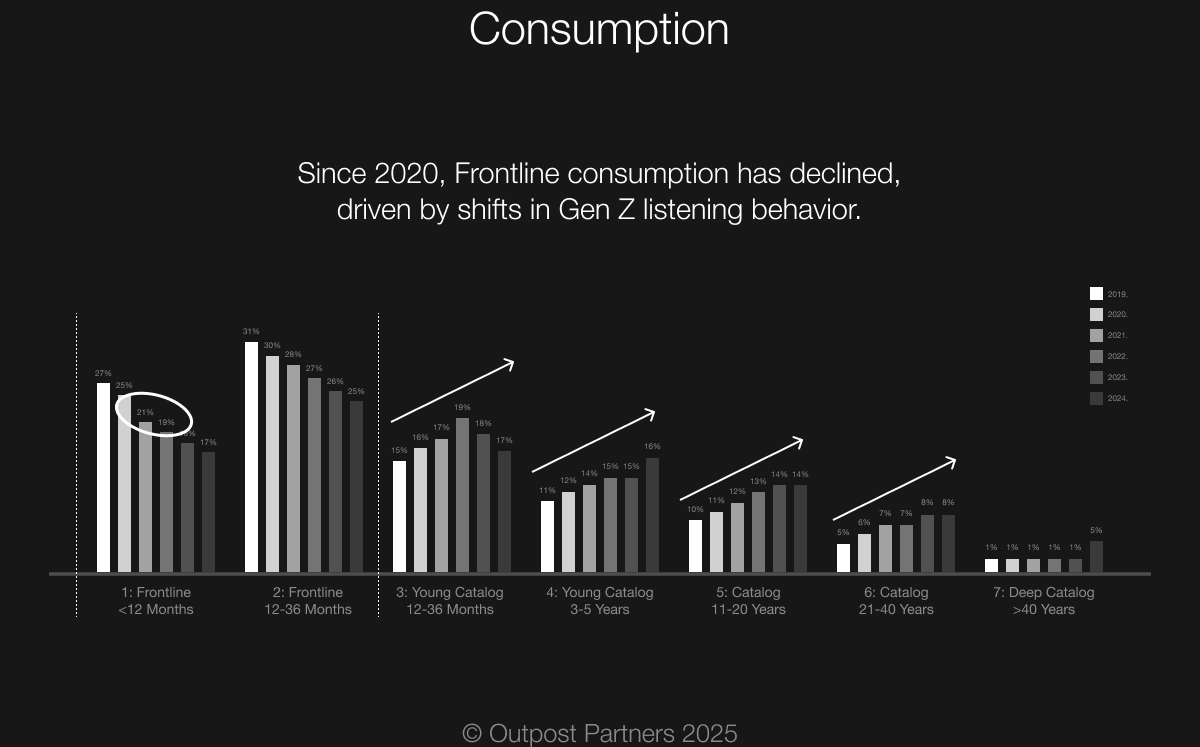

The music streaming market gained momentum in the 2010s, driven by a wave of new users and an appetite for music tailored to the streaming environment. Around 2015, user-friendly distribution platforms made it easier than ever for artists to upload their work. New releases flourished, and audiences explored the expanding features of DSPs. Frontline music dominated—just as it had during the eras of physical sales, radio charts, and traditional promotional campaigns.

That trend, however, has reversed in recent years. Today, Catalog music is consumed more than Frontline releases. This shift becomes clear when examining streaming data. For example, in the GSA2 region, the share of Frontline consumption dropped by 4% between 2020 and 2021, marking a turning point in listening behavior. While this data comes from a single Western market, it reflects a broader trend. Frontline music is generally driven by a younger audience, primarily Gen Z. Millennials, by contrast, tend to focus more on recent Catalog, particularly music released in the past 11 to 20 years, which has steadily grown in consumption over the last five years.

Several factors are driving this shift in consumption, including easier access to music and algorithmic discovery. We identify two key turning points:

As a result, a smaller share of total monthly streams now goes to Frontline music. It’s important to note that consumption does not equal attention or awareness. A large portion of both Catalog and Frontline streams comes from passive listening.3

These developments pose major challenges for the industry, especially when it comes to breaking new hits and building the Catalog of tomorrow. In mature Western markets, several trends are shaping the current environment:

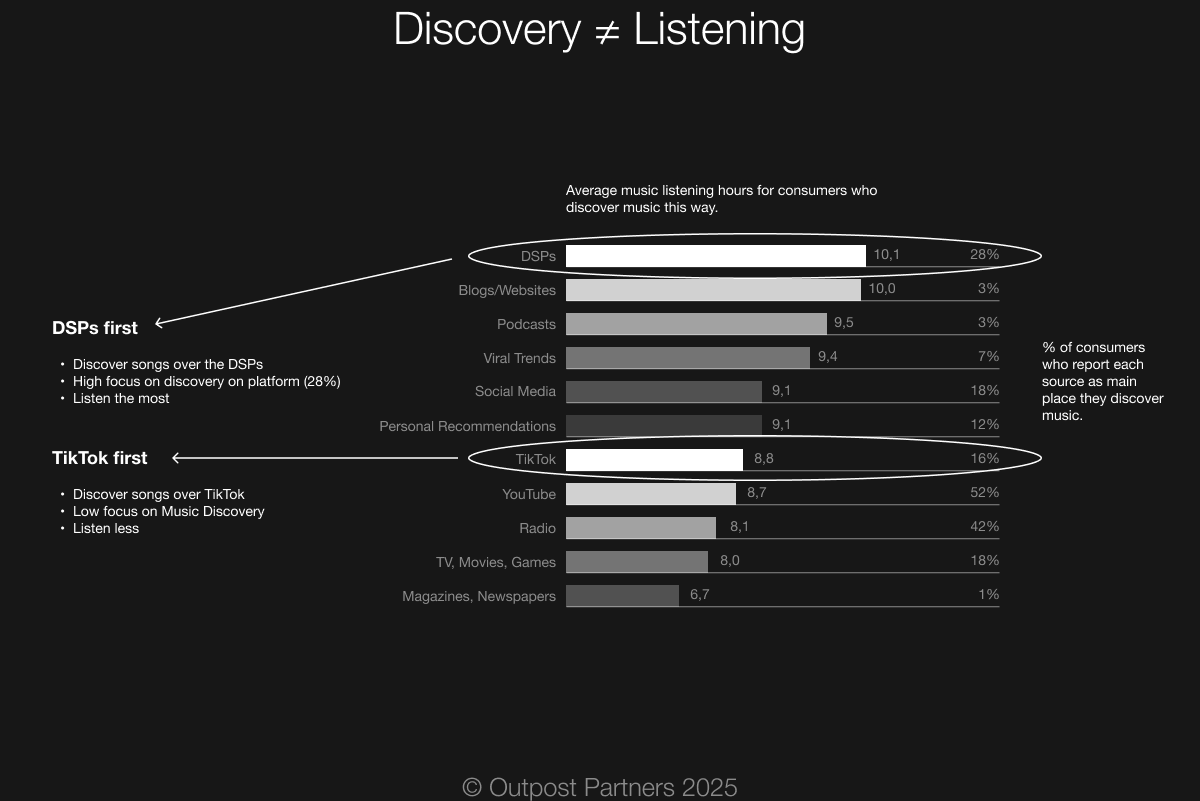

“Discovery” (finding) and “listening” (consuming) are often used interchangeably, but they are fundamentally different actions with distinct goals. Discovery is about exploration and finding something new or unexpected. Listening is about engagement and enjoying a track, whether it is already known or recently discovered. Discovery tends to happen quickly, while listening is slower and more focused.

The main place where people discover music has shifted. Most Millennials still find new music through digital streaming platforms. Gen Z, on the other hand, primarily uses TikTok for discovery. Among DSP users, 28 percent say they discover music on the same platform where they listen—and they stream the most, averaging 10 hours per week. In contrast, only 16 percent of users consider TikTok their main source for music discovery, and this group streams less overall, averaging eight hours per week. This suggests a weaker link between discovery and actual listening.

Millennials tend to explore, listen to, and save new music all within one platform. This creates a higher rate of conversion from discovery to listening. However, this group tends to focus more on Catalog than Frontline releases. Gen Z splits these actions, often discovering songs on TikTok but listening to them later on streaming services. This separation, combined with shorter attention spans and more passive listening habits, contributes to the current challenges in music discovery.

Worth noting: TikTok tried to build its own streaming service but shut it down after 1.5 years at the end of 2024. Instead, it added a feature that lets users transfer songs to their preferred music app.5

With the rise of streaming, passive listening has become more common. This includes listening to music in the background while watching short-form content, studying, cleaning, reading, or engaging in any other primary activity. In this context, hearing new music is not considered discovery, as the user is not actively seeking it out. It may also not qualify as active consumption, since the listener may be only partially aware, or not aware at all, of what is playing.

Passive consumption is driven by several factors:

This shift challenges the traditional dynamic between artists and fans. Building a fanbase requires attention. It also raises the importance of platforms and their algorithms, which now play a key role in deciding what gets shown to users. As passive and Catalog-based listening increases, Frontline marketing becomes more difficult.

Traditionally, youth drive pop culture. The age group between 14 and 19 consumes more movies, music, and sports than older demographics, spending time in their formative years developing identity and culture. Each generation creates its own idols, music genres, and trends. They also shape the entertainment market by consuming more content than older age groups.

People tend to favor music that was popular during their adolescence and early adulthood (typically teens to early twenties), as seen in the consumption patterns of Millennials described earlier. Music reflects generational identity, helps shape it and sustains it over time. Preferences formed during youth are long-lasting.10

Gen Z was the first generation whose identity formation during late childhood and adolescence was strongly influenced by digital platforms, especially social media. Today, they use products, brands, and aesthetics in content to signal identity and align with social groups. Lifestyle branding and values-based marketing, such as sustainability and inclusivity, play a major role in shaping their preferences. Identity develops online today and continues to evolve within digital environments.11

Media consumption and experience, through movies, albums, and interactive games, play an important role in this process. What we watch, listen to, and emotionally connect with can stay with us over the long term, often forming the basis for lasting fandom. Music is one of the most powerful imprinting tools12. Encoding media into memory depends on factors such as exposure time, emotional intensity, repetition, novelty, and the surrounding context in which it is consumed.

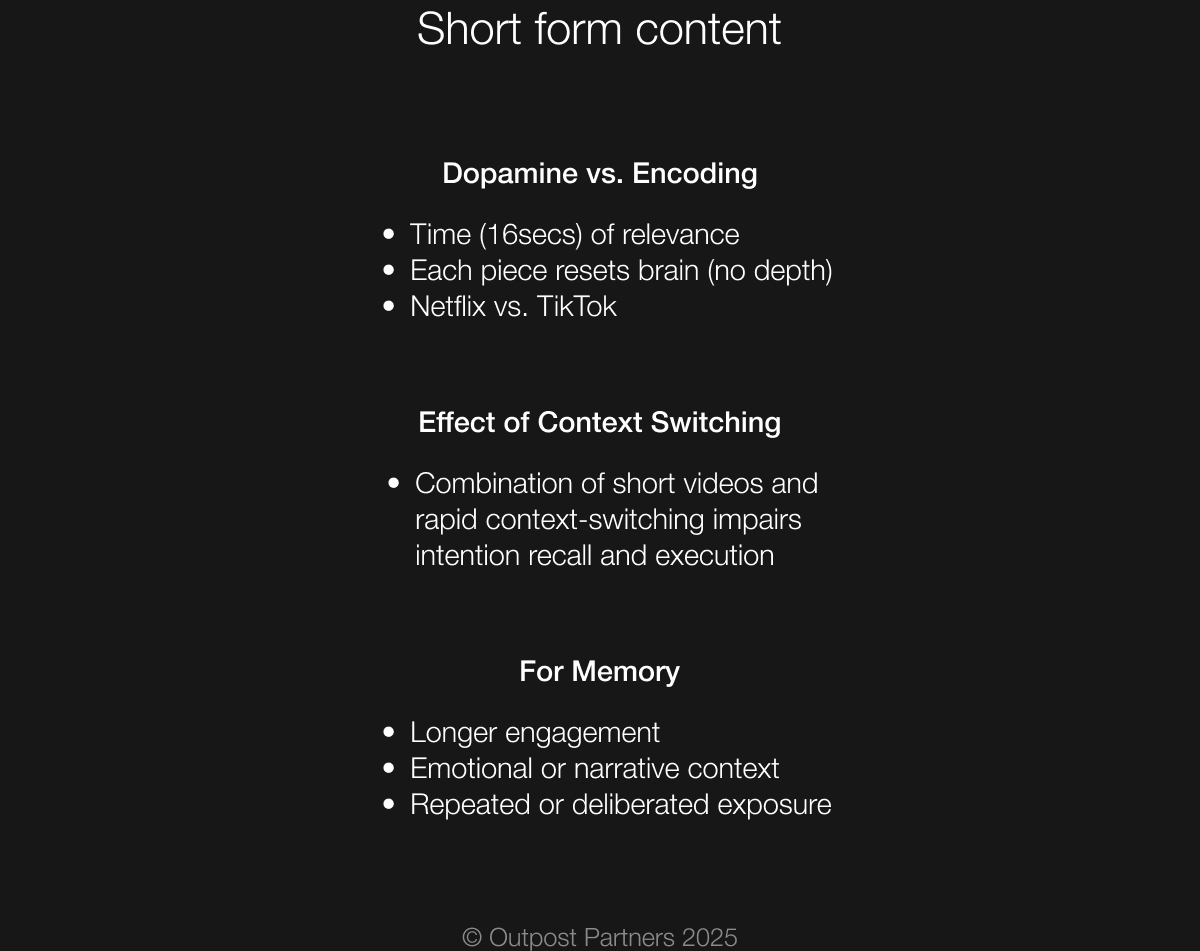

One of the main challenges in music marketing today is Gen Z’s shift toward short-form content. To make short-form content memorable over time, it needs to carry emotional depth. This is difficult to achieve within an exposure window of just 10 to 15 seconds. When short exposure is combined with low repetition (of the same content) and limited context (to the environment in which the content is consumed), it becomes harder to form lasting impressions—making it more difficult to market new music effectively.

The process in short: We see short-form content on the phone and cognitively understand what we are watching or listening to. The novelty of each new piece triggers a small reward in the brain, often in the form of dopamine. But then we swipe up to the next video, which resets us into our initial state. The information, content, or song consumed just seconds before is hardly remembered. This effect makes it harder than ever to break new music, because songs are experienced briefly, with little repetition or emotional context, and are quickly forgotten as users scroll past them.

As creators and marketers try to bridge the gap and generate virality to get picked up by the algorithm, users are exposed to more clickbait or even shocking content overall. Shocking news or content can trigger an emotional reaction strong enough to make someone click, watch, or listen. It is the same effect that triggers doomscrolling16, a habit first observed during the COVID pandemic.

But short-form content can break that pattern and still be memorable. It can even become a vital part of pop culture, as seen in widely remembered memes over the years. For example, TikTok marketing often relies on repetition through user-created videos. Each video is different but follows the same structure, with different people doing the same activity (for example, dancing), while including the same song. This increases exposure frequency until the song becomes viral and, eventually, a hit.

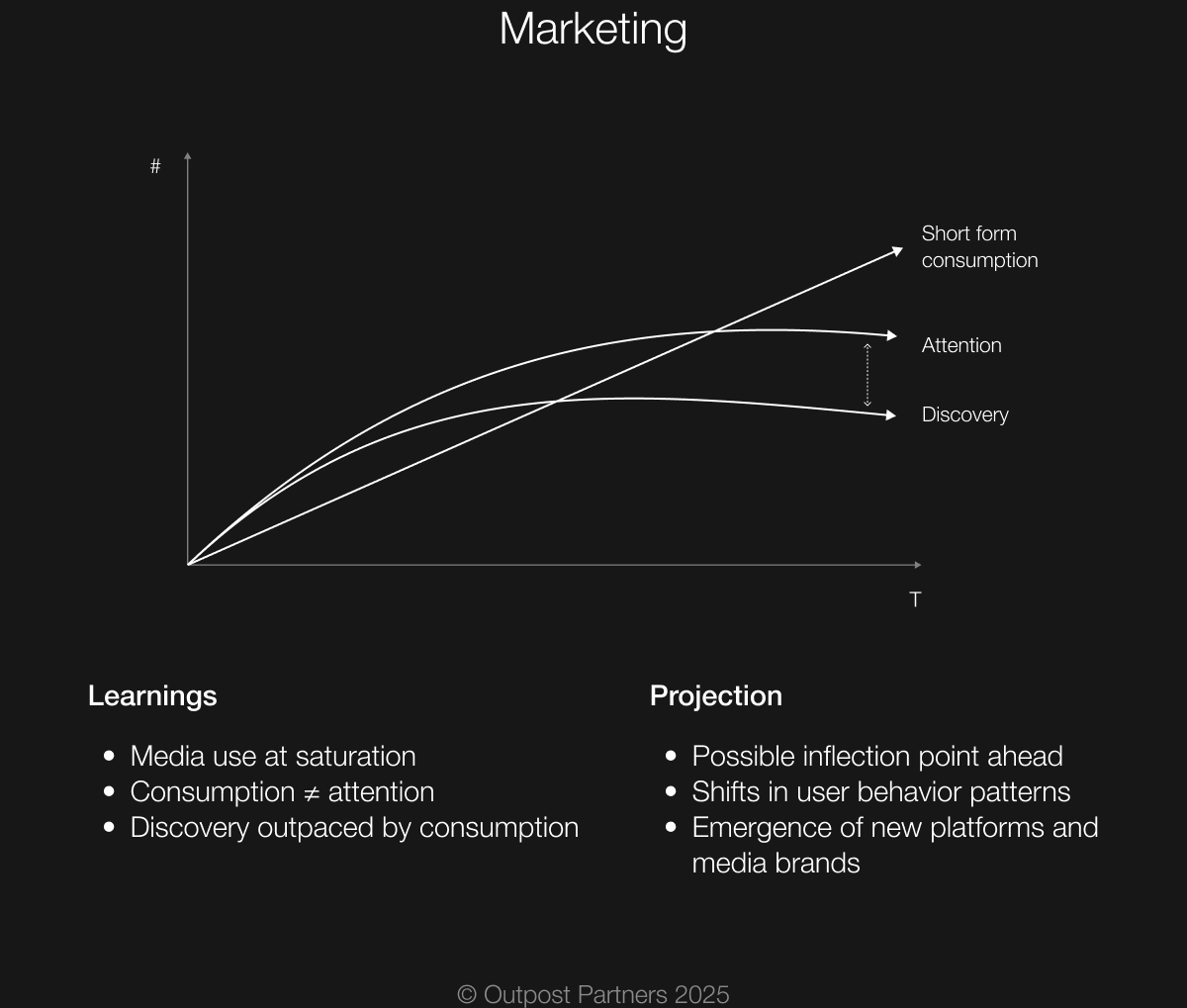

As the influence of short-form content grows, from discovery to marketing, it is worth examining the overall composition of media time spent and what it means for music, especially in the context of passive consumption.

Time spent on media:

In the last decade, U.S. digital media grew faster than traditional media declined (TV, print, radio), expanding total media time to around 12 hours per day17. That trend has now shifted. For the first time, media time has plateaued in 2024. The growth of digital has only just offset the decline in traditional media18. The growth in users of social media platforms is also slowing, and time spent on social media is even projected to decline by 202719. The current projection for 2025 shows a global decline of 0.3 percent in media time, and 1.8 percent in the U.S20.

Among the many factors driving this shift, such as the economic pressures of a recession, is the saturation point of digital device usage: In the U.S., nearly everyone now owns a smartphone, tablet, or connected TV.21

For years, we dedicated more and more time to media, allowing newer forms to grow (short-form, streaming, gaming) while older ones declined. Now that total media time is stagnating, we can expect greater competition between media formats. Music, especially when passively consumed, is well suited for this environment. It easily fits into the background of other activities. The downside is that discovery suffers, because the music being consumed is often not actively listened to. In many cases, the listener doesn’t know the artist or even the track name. As short-form content takes up more share, the question is whether this fast-paced format can lead to sustainable fandom.

A lot of artists who were popular around the early 2020s are no longer streaming as well as they once did. While their Catalog tracks still perform well, their new releases don’t seem to connect with younger audiences. This isn’t necessarily a new phenomenon, but the speed of both their rise and decline is striking, considering these artists were producing record-breaking numbers just a few years ago.

The current development we are seeing:

What this currently means for music marketing:

In the long run, the saturation of devices, streams, and media time in the Western world may signal a broader inflection point. While it is still too early to predict what this shift will bring, it is likely to be driven by a generational change. Gen Z’s habits have tipped the balance toward short-form content, but it remains unclear whether future generations will adopt the same patterns or how they will manage media and short-form consumption, especially as the effects of overconsumption and addiction become more visible.27

Historically, shifts in user behavior have opened the door for new content platforms to emerge. As older platforms try to adapt, new media and music brands are born and often rise with the change.

The rise of AI has sparked widespread excitement across industries, and the creative sectors are no exception. From text to video to voice synthesis, generative models have rapidly expanded both creative and commercial possibilities. Music is emerging as one of the most active and visible frontiers.

The underlying models that power music generation, software capable of creating music from prompts, are typically trained on large datasets. In most cases, this includes music catalogs that require proper licensing and a fair remuneration model. Many platforms do not have these licenses in place, leading to lawsuits28 and legal disputes with rights holders. These licensing and training issues currently dominate much of the industry conversation.

To several sectors, including venture capital, music and AI seem like a perfect match. Over the past 12 to 18 months, more startups have launched in generative music and developed AI-powered digital audio workstation (DAW) than in nearly any other Music Tech vertical, rivaled only by NFT marketplaces during the last crypto bull run.29

This report does not focus on the legal and licensing debate. Instead, it explores what these platforms enable for users and what that means for the recorded music industry. While the field is too broad to cover in full, this section examines the early impact of AI on the music rights market and highlights key observations from the first wave of innovation.

Despite its impressive technical capabilities, generative music lacks one critical dimension: the presence of an artist or artist brand—a core element in how music fosters identity, belonging, and culture. People tend to prefer music from artists whose perceived personalities align with their own, demonstrating that identity, not just sounds, is central to engagement and fandom30. Artists represent a stance, emotion, or worldview that listeners relate to, emulate, or even integrate or adapt. In this sense, idols don’t just produce music—they carry meaning, and their songs serve as vehicles for emotional and cultural imprinting.

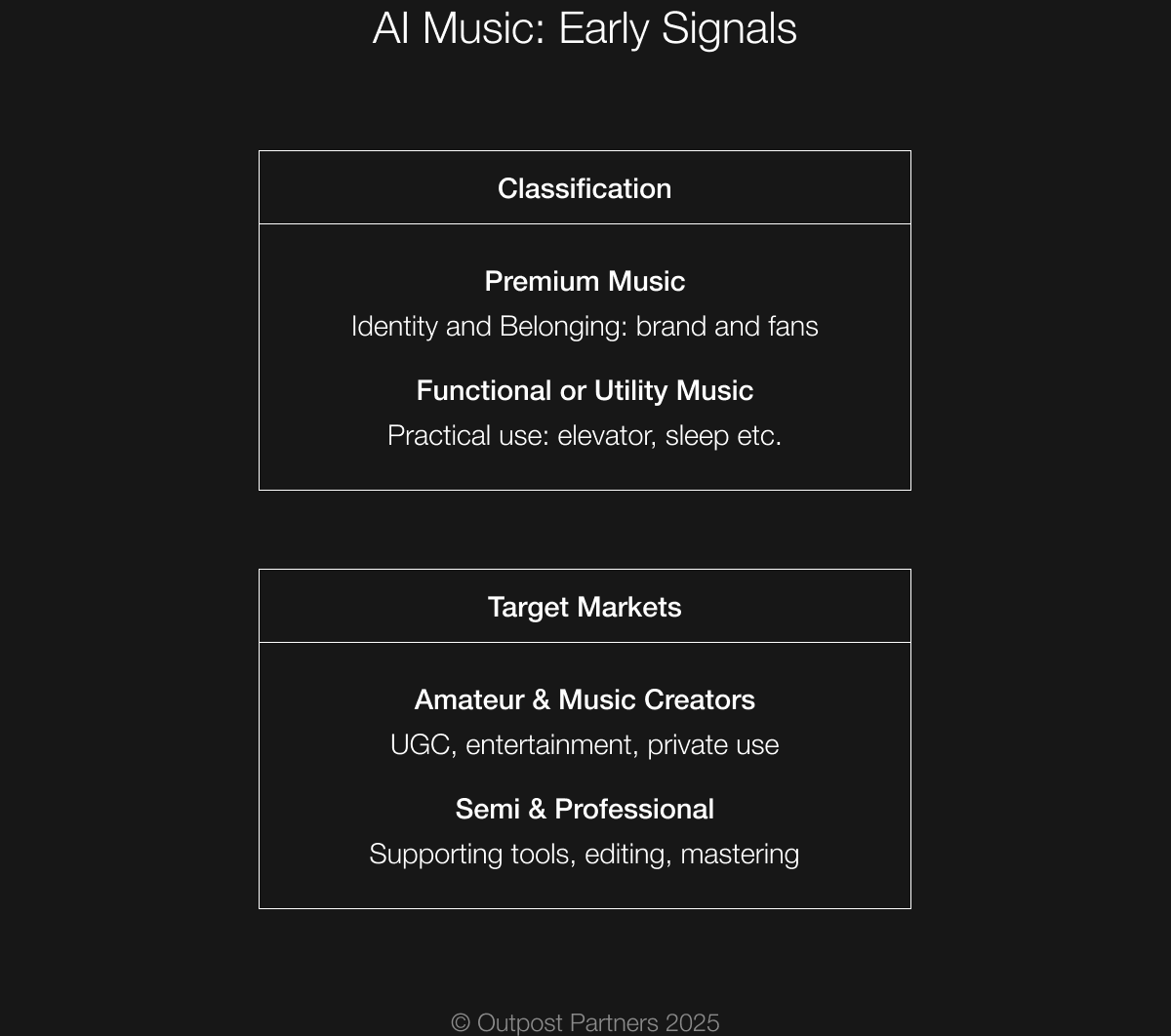

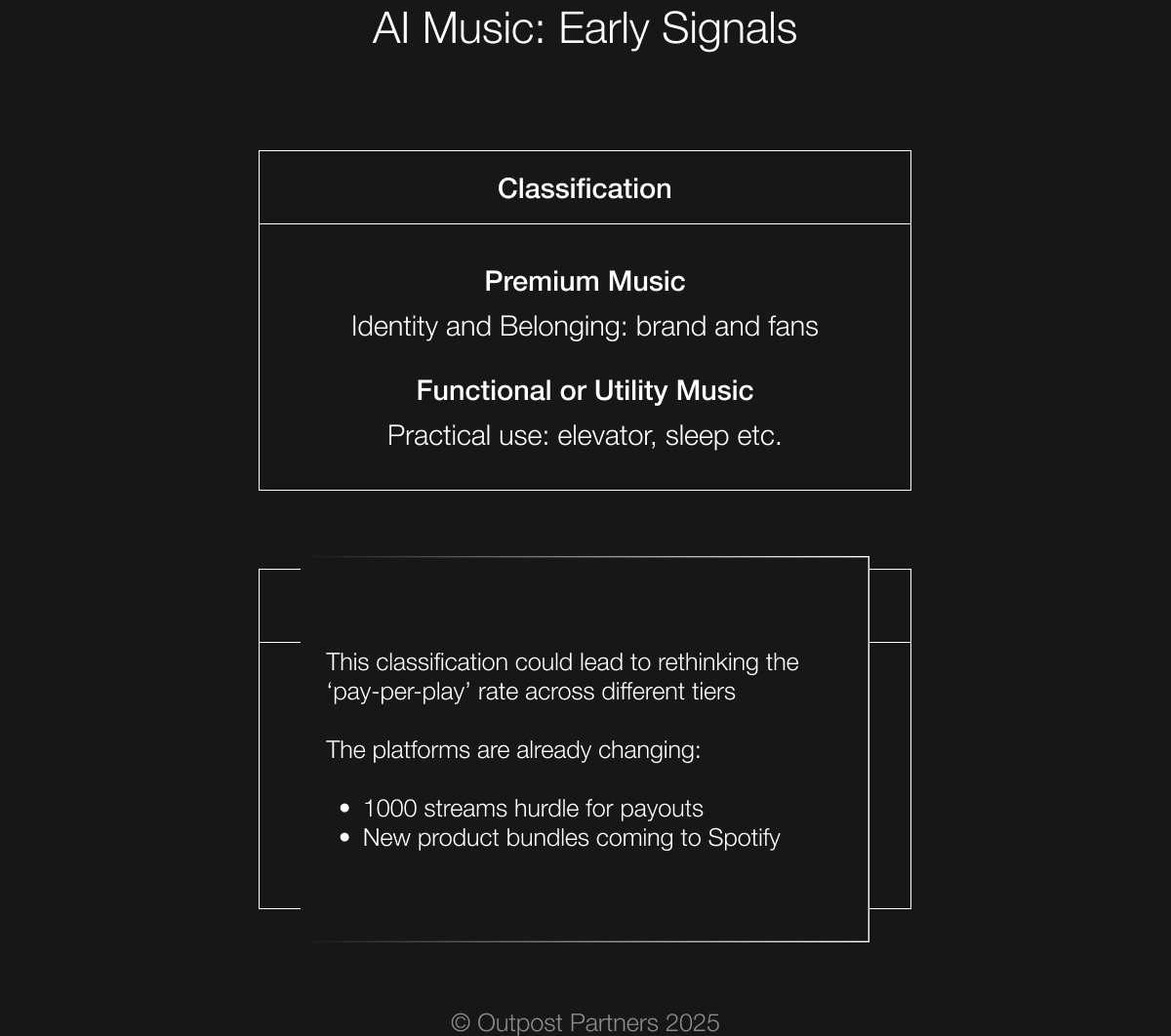

Prompt-based generative music, at least in its current form, does not offer that. It lacks this symbolic weight that allows music to serve as a marker of identity or community. What it does offer is functional value: it can help us sleep, focus, relax, or serve as unobtrusive background sound—whether on phones, in homes, in elevators, on hold lines, or behind video content. While music has historically served functional purposes across cultures, generative music can now fulfill a broader range of use cases, offering experiences that are more personalized, adaptive, and context-specific than ever before.

At Outpost, we distinguish between Premium Music – artist-driven, brand-led, and designed to foster identity and belonging for fans – and Functional (or Utility) Music, which is unbranded, purpose-oriented, and optimized for use cases where identity and authorship are secondary. Technically, both types of music can be created by humans or AI. In practice, however, Premium Music is still primarily human-made, while Functional Music is increasingly generated by AI.

The second distinction worth exploring focuses on the people creating the music. Broadly speaking, we see two major groups emerging:

While both groups have always existed, the amateur and casual creator segment is growing rapidly—largely fueled by the rise of smartphones, mobile apps, and accessible creator tools. With AI-powered music platforms entering the space and making music creation easier than ever, we are entering a new phase of growth—one in which a significant number of casual users could begin moving up to become semi-professional or even professional artists.

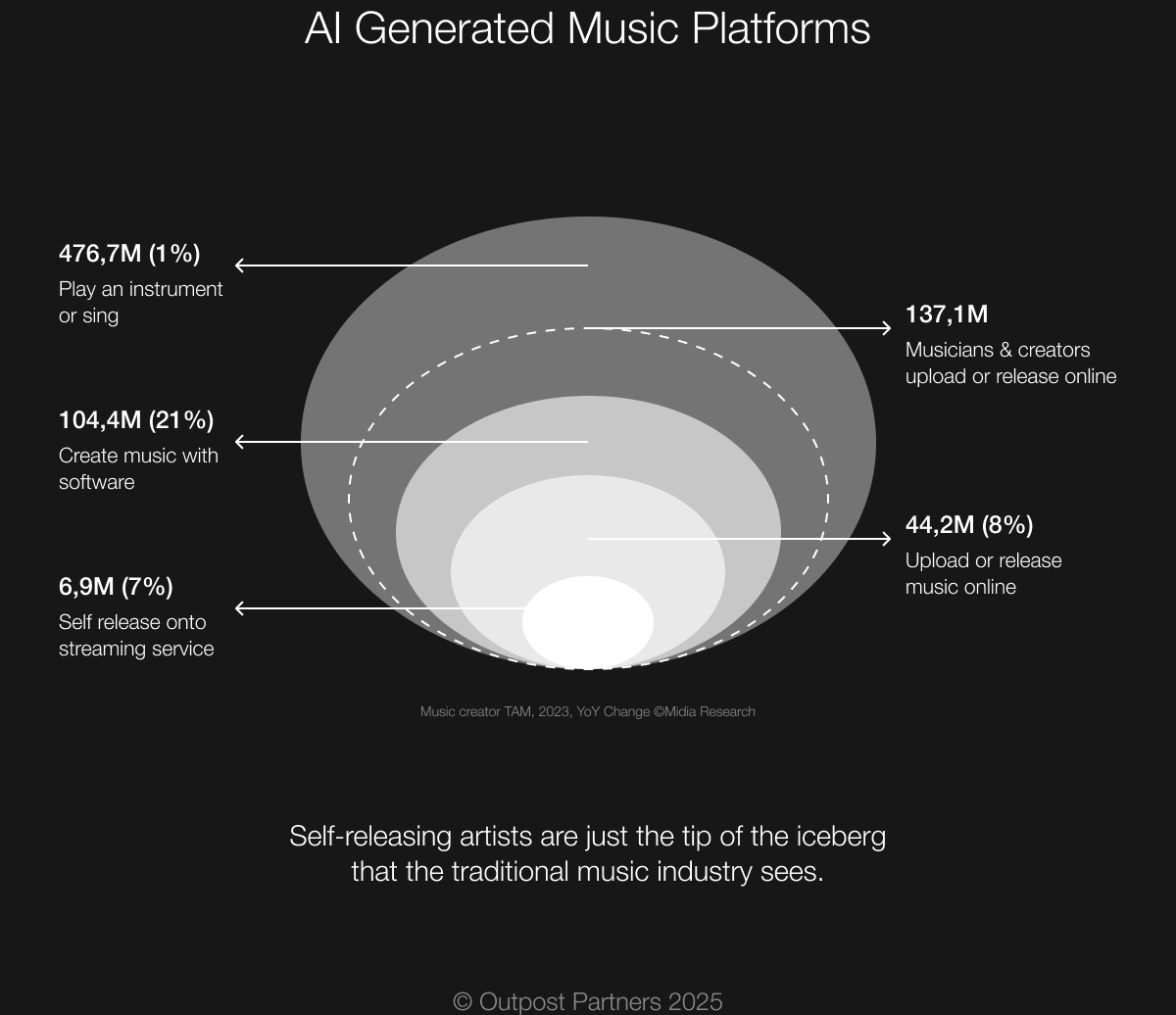

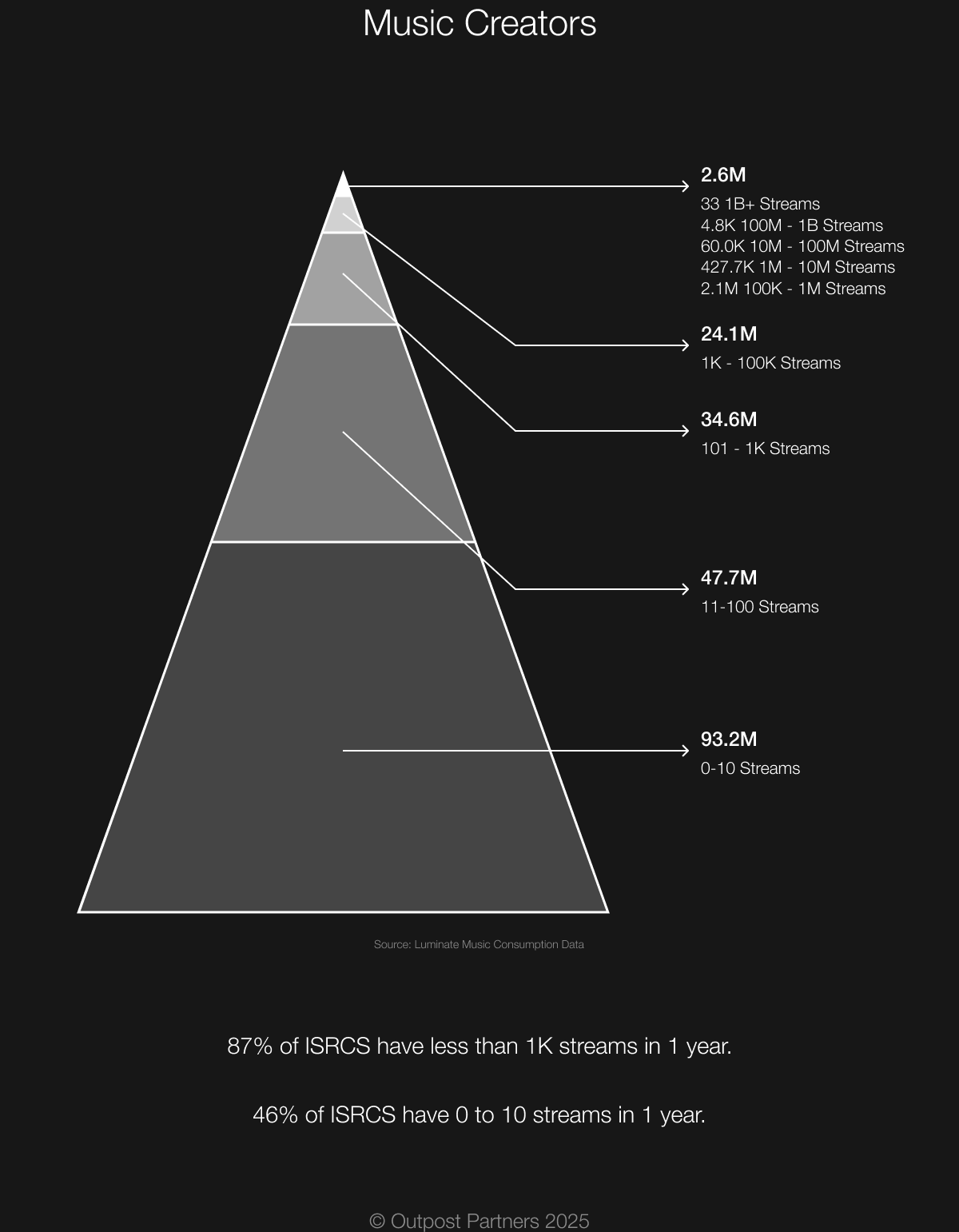

Roughly 500 million people around the world play an instrument or sing. While that number has remained relatively stable over time, about a third of them now share their music online. These uploads span a wide range—from professional productions to simple audio recordings uploaded to platforms like YouTube, TikTok, or SoundCloud.

In 2023, approximately 100 million people produced music using software—a group commonly referred to as Music Creators. This marked a 22% increase over the previous year. Of these, 44 million released music online, an 8% year-over-year increase. Within that group, around 7 million creators released music independently onto DSPs, mostly through distribution aggregators.

While this group has driven a massive increase in the volume of new releases, it still represents only 6–7% of all digital Music Creators. The gap between those who produce, those who release, and those who self-release onto DSPs highlights a key insight: the desire to create does not necessarily translate into the desire to distribute or publish.

Notably, these numbers were captured prior to the widespread adoption of AI tools, which significantly lowered the barrier to entry. AI-powered DAWs and creation tools are now accelerating this trend long term and onboarding even more users into the ecosystem.

As the number of Music Creators continues to grow, so does the volume of music released on streaming platforms. Spotify now hosts around 200 million tracks, with approximately 99,000 new ISRCs31 uploaded each day—a dramatic increase compared to just 5 years ago. The majority of these uploads come from distribution platforms like DistroKid, where users pay a flat fee to release music. By our estimates, less than 5% of all songs are distributed by major labels or their affiliates; the rest come from the independent sector, small labels or direct uploads by artists.

But volume doesn’t equal attention, and scale doesn’t guarantee reach. Of the 200 million tracks on Spotify, 46% have zero streams, and 87% have fewer than 1,000 streams per year. The classic power-law distribution still applies: In the U.S. of all artists with more than 100M streams in the first half of 2024, over 90% were distributed by the major labels32. And although the major labels supply less than 5% of total content, just one—Universal Music Group—still holds around 30% of overall market share33.

Spotify’s content economics increasingly resemble YouTube’s open content model rather than a curated digital record store—where the vast majority of the long tail remains invisible, while a small number of top tracks drive the bulk of streams. This open infrastructure creates opportunities for bad actors to exploit the system, from stream manipulation to fraudulent uploads and copyright abuse.

The rise of AI-powered creation tools, combined with the ease of uploading music to platforms like Spotify, has introduced significant challenges for DSPs. Streaming fraud, where bad actors use bots, click farms, or stolen user credentials to inflate play counts, is not new. Initially, this was a tactic used by artists or labels to boost their visibility and to get onto charts and playlists. Over time, the practice shifted toward instrumental and background music, with malicious actors using distribution platforms to upload content and capturing micro-revenue at scale.

Now, generative AI has elevated streaming fraud to a new level. Offenders no longer rely on artists, brands, or legitimate partners, they can autonomously generate massive volumes of audio and visual content. This content floods DSPs, while coordinated bot networks are programmed to stream it strategically—for example, by automatically creating, streaming, and deleting playlists to avoid detection— diverting royalties at scale.

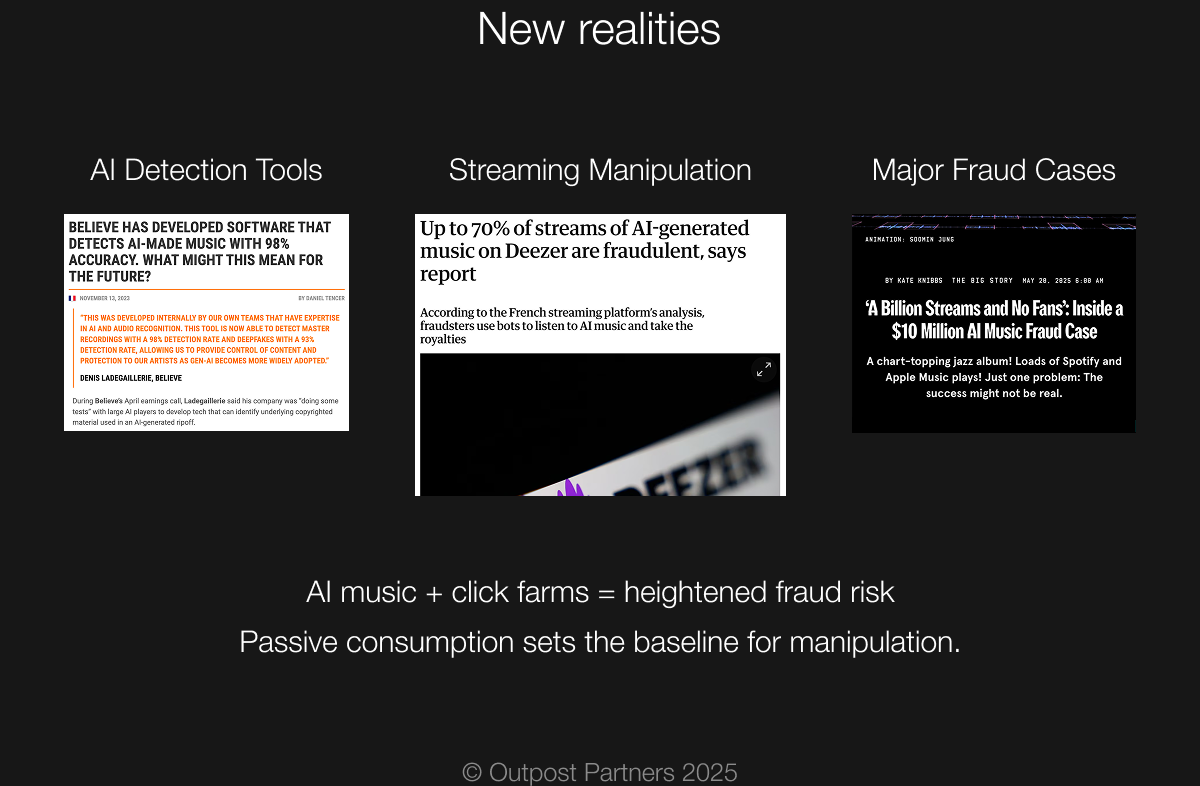

Detection is becoming harder. In some cases, bad actors are creating fully artificial artist personas, complete with Instagram pages, paid ads, and streaming manipulation systems—blurring the lines between real and synthetic. As passive listening grows and Frontline consumption declines, this creates a dangerous dynamic: fraudulent content begins to eat into the attention and payouts of real, and emerging artists. In one recent case, a North Carolina-based malicious actors reportedly uploaded hundreds of thousands of AI-generated tracks, each streamed just enough times via bots to avoid detection, earning over $10 million in royalties from DSPs.34

The most effective way to combat AI-generated content may be through AI itself, and DSPs are beginning to upgrade their infrastructure accordingly. French distributor Believe Digital recently announced the launch of AI Radar, a detection tool that can identify AI-generated master recordings with 98% accuracy and deepfakes in 93% of cases. The company stated it does not intend to distribute any content that is 100% AI-generated.35

Meanwhile, Paris-based streaming service Deezer revealed that as of April 2025, around 18% of the tracks uploaded daily—more than 20,000 songs—are created using artificial intelligence. That number has doubled in just three months, up from 10,000 in January36. Although AI-generated tracks make up only about 0.5% of total streaming consumption, Deezer stated that roughly 70% of the streams attributed to them are fraudulent37. While the DSP has not banned AI-generated content, it is using proprietary systems to filter such tracks from playlist recommendations and promotional surfaces, significantly reducing their visibility to users.

Other platforms like YouTube are also updating their policies. While the platform already had measures in place against mass-produced, inauthentic and repetitive content, it has now introduced stricter rules targeting “AI slop” – a term used to describe low-quality media generated with AI tools. This type of content will no longer be eligible for monetization.38

The gap between premium music made by human artists and utility music generated by AI is likely to grow, as AI content continues to enter DSPs at high volume. Spotify has already responded by changing its payout rules: as of 2024, a track must reach at least 1,000 streams within 12 months to earn royalties. The company also announced a new pricing tier, launching in 2025, that includes higher audio quality, more content, and extra features for about $6 more per month.39

One proposed solution to improve fairness in the streaming economy has been the user-centric payout model, where a listener’s subscription fee is distributed only among the artists they actually stream—rather than pooled and split proportionally across the platform. While this model has been widely discussed, only SoundCloud has implemented it to date, and even then, only for artists distributing through SoundCloud’s infrastructure and only for streams on its own platform.40

An alternative approach: instead of focusing solely on the user, platforms may begin to differentiate between types of content. This could involve tiered royalty rates—for example, paying a higher rate for premium music from verified artists and a lower rate for AI-generated utility music. Another variation could be based on consumption type: assigning higher payouts for active listening (from personal playlists, libraries, or direct searches) and lower rates for passive listening (from algorithmic playlists, radio functions, or background use).

But while generic and artificially created music is breaking into the market, premium music is not going anywhere, and might become more valuable along the way. Universal Music’s Chief Digital Officer, Michael Nash, stated earlier this year that internal consumer research showed around 50% of listeners are interested in AI and music—primarily for utility and discovery. However, the vast majority, around 75%, said that real artists matter most to them41, underscoring the emotional connection built through their identities and stories.

To recap some of the the statements we’ve identified as valid today:

Consumption

Media consumption now fills most of our waking hours, whether actively or passively. Short-form content has made it easy to occupy every free moment — in the elevator, during breaks, or while sitting on the sofa. This shift has had measurable effects. Over the past 20 years, the average human attention span has dropped from 2 minutes and 30 seconds to just 47 seconds in 2024 — almost exactly the average length of a TikTok video42.

For music marketing, the challenge is not only the short-form format itself but also the algorithms behind it. TikTok’s feed, for example, is driven by content performance rather than a user’s social or interest graph. As a result, building a following is difficult, since followers are unlikely to see future posts. Content is surfaced not because of who created it, but because the algorithm identifies it as similar to previously engaging videos. This algorithm is likely to keep the platform growing in the near future: ByteDance just announced record revenues43, and TikTok users now spend nearly twice as much time with music on the platform compared to Instagram44.

While fragmented attention and fewer Frontline streams challenge newcomers and small labels, we expect them to be less of an issue for market leaders. Major record labels will continue to do well, as they have adapted their business model: rather than developing artists from scratch, they increasingly sign, fund, and amplify those already on the rise. Their distribution arms (e.g., Sony’s Orchard) give them both reach and valuable insights. They may no longer secure lifetime rights as they once did, but this shift de-risks their investments and makes returns more predictable.

But if attention fragments further, consumption itself may shift. Younger audiences already “listen on TikTok,” looping 15-second hooks instead of full tracks. At the same time, platforms have optimized for video performance and retention rather than music discovery. Discovery is equally fragmented — and on DSPs almost entirely algorithmic, favoring passive listening over active exploration. While everyone talks about “superfans,” fandom has largely become a by-product at the platform level. The paradox will only deepen: technically, we have all the world’s music at our fingertips; practically, we don’t know whom to follow — or how to become a real fan of something new.

AI Music: Changing Dynamics

At Outpost, we believe that purely prompt-based music is likely to trend toward a price point close to zero. It will become an added value—bundled and integrated into existing solutions, either within DAWs for semi-professional and professional users or editing platforms like Adobe Premiere Pro or Final Cut for creators looking for utility music. Unless these tools evolve into fully standalone products, it will be difficult for them to live up to the hype.

We’re beginning to see signs of this shift. AI-powered DAWs are moving beyond basic prompt-based generation, adding more advanced features to support semi-professional users. Some companies are already repositioning. For example, generative AI company Suno recently acquired WaveTool to expand its capabilities for professional songwriters and producers45.

We expect the initial excitement around amateurs and casual Music Creators as a large addressable market to cool off. Prompt-based music has novelty, but it lacks long-term engagement. While AI does make it possible for anyone to generate music with a few clicks, the idea that billions of people will regularly create music—and that this represents a major market opportunity—feels far-fetched. That narrative appears to be driven more by investor optimism than by real user behavior or demand46.

However, the market of semi-professional creators could see meaningful growth, as more users are onboarded through AI-powered tools. This smaller but more dedicated group is typically more willing to pay for software, invest in building their artist brand or project, and actively distribute their music. That makes them a strong target audience for tools that streamline workflows and support more serious creative output.

The “Instagram moment” for music—where everyone becomes a creator—has not arrived, and it may not come as quickly as some expect. With photography, the distinction between an artistic shot and a quick picture with your grandmother can coexist naturally on the same platform. In music, that divide is more rigid: artistic output and functional content serve different purposes and are experienced differently. For now, most people don’t feel the same ease or motivation to casually create and share music as they do with photos.

Robot land

There is currently a strong focus on AI at the content creation stage, particularly around video production and advertising. Today, it takes a fraction of the time it took five years ago to generate video content, set up distribution channels through social accounts, and create the matching ads and launch campaigns. While this applies across industries, media and music stand out because they monetize attention directly. That makes them more vulnerable to exploitation through bots and fraudulent schemes.

Views and streams are fully monetized if the platform cannot detect or does not act against bot-driven activity. This is not the case in other industries where monetization depends on subscriptions, physical products, or services—bots do not buy merchandise. For this reason, music and media are especially attractive to bad actors. With AI, they can control both ends: content creation and consumption, while monetizing the activity in between.

The market is poised to grow: Spotify, for example, pays royalties on a pro-rata basis independent of the rights holder, and with around 60% of users still on the free tier, it has ample room for conversion. Within the complex metadata system, streams and revenue are often misallocated, which has led to the emergence of legitimate players. Startups like Beatdapp47 and Mogul48, for instance, help rightsholders identify and recover missing royalties.

As a result, we are likely to see more content, more bots, and more advanced manipulation — but also smarter detection systems from both platforms and third parties, increasingly powered by AI. Or, as our chief designer puts it: we are now in robot land.

Thank you.

In case you are interested in collaborating please reach out over: contact@outpost.partners

Footnotes:

1 https://www.pewresearch.org/short-reads/2019/01/17/where-millennials-end-and-generation-z-begins

2 GSA refers to the German-speaking region comprising Germany, Switzerland, and Austria.

3 See 2.3

4 https://www.midiaresearch.com/blog/are-we-reaching-peak-fandom

5 https://www.wsj.com/tech/tiktok-to-shut-down-music-streaming-service-753c71fd

6 https://www.pewresearch.org/internet/2024/03/11/how-teens-and-parents-approach-screen-time/

7 https://www.pewresearch.org/internet/2023/12/11/teens-social-media-and-technology-2023/

8 Luminate, 2024 Year-End Music Report, January 2025. https://luminatedata.com

9 See 4.1

10 https://gss.norc.org/content/dam/gss/get-documentation/pdf/reports/social-change-reports/SC37.pdf

11 https://digitalcommons.unl.edu/cgi/viewcontent.cgi?article=1188&context=dissunl

12 Ren, Y., Mehdizadeh, S.K., Leslie, G. et al. Affective music during episodic memory recollection modulates subsequent false emotional memory traces: an fMRI study. Cogn Affect Behav Neurosci 24, 912–930 (2024). https://doi.org/10.3758/s13415-024-01200-0

13 https://www.wsj.com/tech/personal-tech/tiktok-brain-explained-why-some-kids-seem-hooked-on-social-video-feeds-11648866192

14 https://www.researchgate.net/publication/368330334_Short-Form_Videos_Degrade_Our_Capacity_to_Retain_Intentions_Effect_of_Context_Switching_On_Prospective_Memory

15 https://hms.harvard.edu/news/making-memories

16 https://www.merriam-webster.com/dictionary/doomscroll

17 Media time can be measured in different ways. In this case, the figures reflect cumulative (duplicated) time and include overlapping usage due to multitasking. Some data points are based on daily activity, others on weekly averages.

18 https://www.emarketer.com/content/us-media-consumption-hits-saturation-point

19 https://www.emarketer.com/content/us-social-network-forecasts-2025

20 https://www.mediapost.com/publications/article/405114/time-spent-with-media-reaches-saturation-declin.html

21 https://www.pewresearch.org/internet/fact-sheet/mobile/

22 https://www.vanityfair.com/hollywood/2022/05/stranger-things-kate-bush

23 https://www.thewrap.com/kpop-demon-hunters-success-couldnt-have-happened-in-theaters/

24 Schwartz, Barry. 2004. The Paradox of Choice: Why More Is Less. New York: Ecco.

25 https://www.ibtimes.com/most-major-movies-next-year-will-prequels-sequels-remakes-report-3745719

26 An example: https://www.newsweek.com/julie-tuzet-responds-fake-video-astronomer-andy-byron-ceo-coldplay-2101618

27 https://www.nature.com/articles/s41598-025-09656-x

28 https://www.gema.de/en/news/ai-and-music/ai-lawsuit

29 See our Music Tech Report 2025: https://outpost.partners/h-content/uploads/2025/07/Outpost-Partners_Music-Tech_2025.pdf

30 https://pubmed.ncbi.nlm.nih.gov/32614219/

31 ISRC: a unique code that identifies individual sound recordings for tracking and royalty purposes.

32 Luminate. 2024 Year-End Music Report. Luminate Data, 2024. https://luminatedata.com

33 IFPI. Global Music Report 2024: State of the Industry. International Federation of the Phonographic Industry, 2024. https://www.ifpi.org

34 https://www.wipo.int/web/wipo-magazine/articles/how-ai-generated-songs-are-fueling-the-rise-of-streaming-farms-74310

35 https://www.musicbusinessworldwide.com/believe-has-developed-its-own-ai-made-music-detector-with-98-accuracy-what-might-this-mean-for-the-future1/

36 https://newsroom-deezer.com/2025/04/deezer-reveals-18-of-all-new-music-uploaded-to-streaming-is-fully-ai-generated/

37 https://newsroom-deezer.com/2025/06/deezer-launches-worlds-first-ai-tagging-system-for-music-streaming

38 https://support.google.com/youtube/answer/1311392

39 https://www.ft.com/content/425cbc57-fa9f-4f51-84ee-1ba57c50a15e

40 https://legacy-community.soundcloud.com/fanpoweredroyalties

41 https://www.musicweek.com/digital/read/umg-s-michael-nash-on-the-velvet-sundown-ethical-ai-and-artist-tools-at-the-ai-for-good-summit/092262

42 https://www.apa.org/news/podcasts/speaking-of-psychology/attention-spans

43 https://www.reuters.com/business/finance/tiktok-owner-bytedance-sets-valuation-over-330-billion-revenue-grows-sources-say-2025-08-27/

44 https://www.thewrap.com/tiktok-users-spend-twice-time-instagram/

45 https://suno.com/blog/suno-acquires-wavtool

46 See our first report for investor bias and TAM sizing

47 https://beatdapp.com/

48 https://www.usemogul.com/

This website uses cookies to improve user experience. To learn more take a look at our Privacy policy.

By selecting "Accept cookies" on this banner, you agree to the use and storage of cookies on your device.